When you hear the word “trust,” you might picture billionaires or multi-generational family dynasties. But you do not need to be ultra-wealthy to benefit from a trust. Anyone who wants control over their assets can benefit from a trust.

In fact, we regularly meet professionals in their 30s who experience a sudden financial windfall, such as a $3 million payout from stock options after their company goes public. While that level of success is exciting, it can also feel overwhelming. A trust can provide structure, protection, and long-term planning for those who have built significant assets earlier in life and want to make thoughtful decisions about what comes next.

In this article, we share:

-

- It’s About Control, Protection, and Clarity.

- Trusts for Everyday Goals

- When Should You Start the Conversation About a Trust?

- How Can Trusts Reduce Income Taxes While Maintaining Control?

- What Role Do Trusts Play in Estate and Gift Tax Planning as Rules Change?

- What Are the Most Common Tax Mistakes People Make with Trusts?

- How Do States Tax Trust Income?

It’s About Control, Protection, and Clarity

Trust planning can make sense for:

-

- Families with minor children

- Blended families (such as couples with children from prior marriages, in-laws, etc.)

- Business owners

- Individuals with life insurance policies

- Families caring for a loved one with special needs

- Individuals with charitable goals

- Couples who want structured estate tax planning

The key is not how wealthy you are. The key is whether you want more control, protection, and clarity around how your assets are managed and distributed.

Trusts are not about surrendering control. When properly designed, you define the rules, choose the trustee, and determine how and when income or assets are distributed.

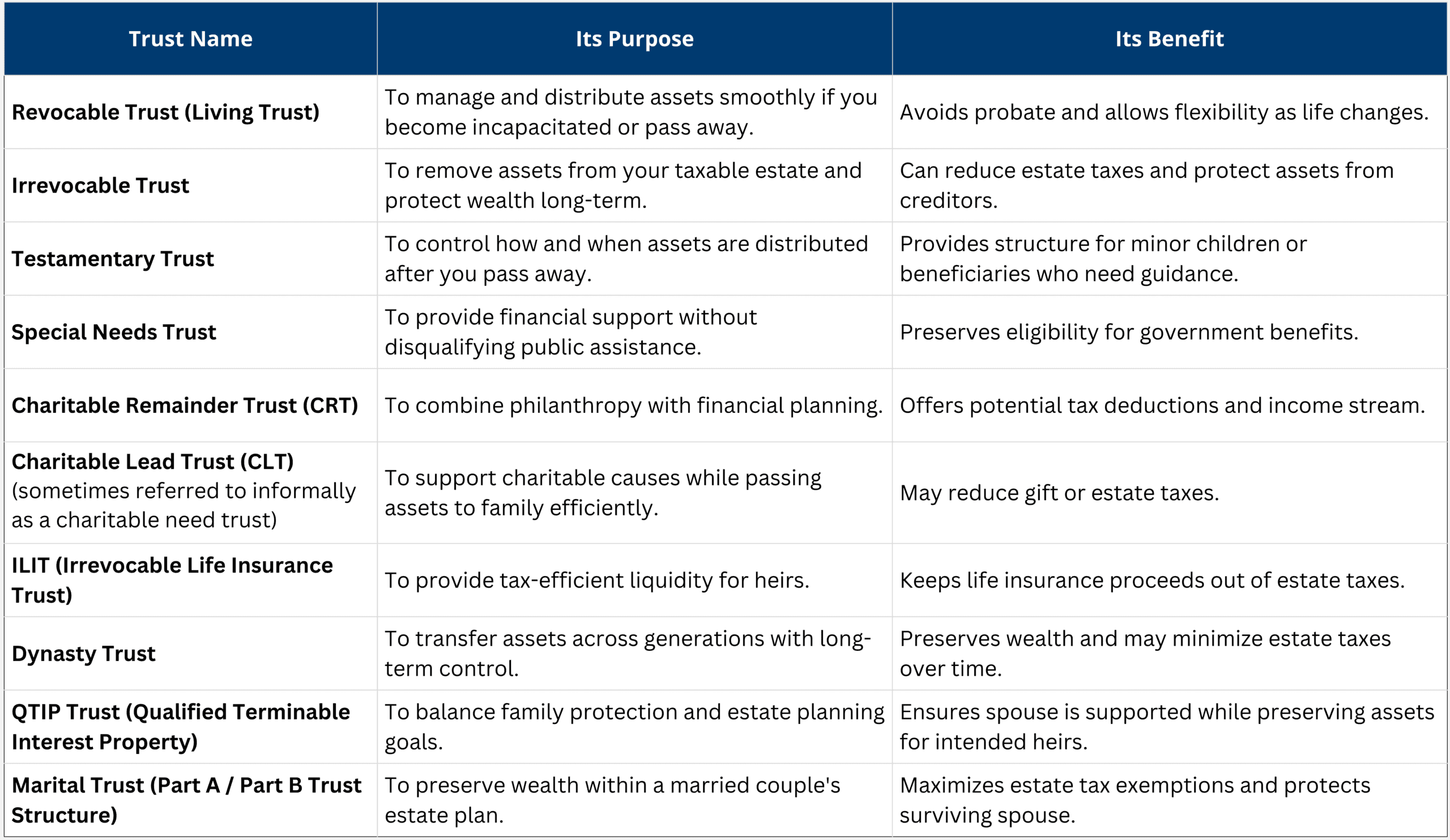

Trusts for Everyday Goals

While trusts can absolutely help someone who receives a large windfall, they are not limited to one age group or income level. In fact, there are many types of trusts designed for different goals, from protecting children to supporting a loved one with special needs or managing life insurance proceeds.

The right structure depends on your family situation, long-term goals, and how you want your assets handled.

Below is a breakdown of common trust types and how they are typically used.

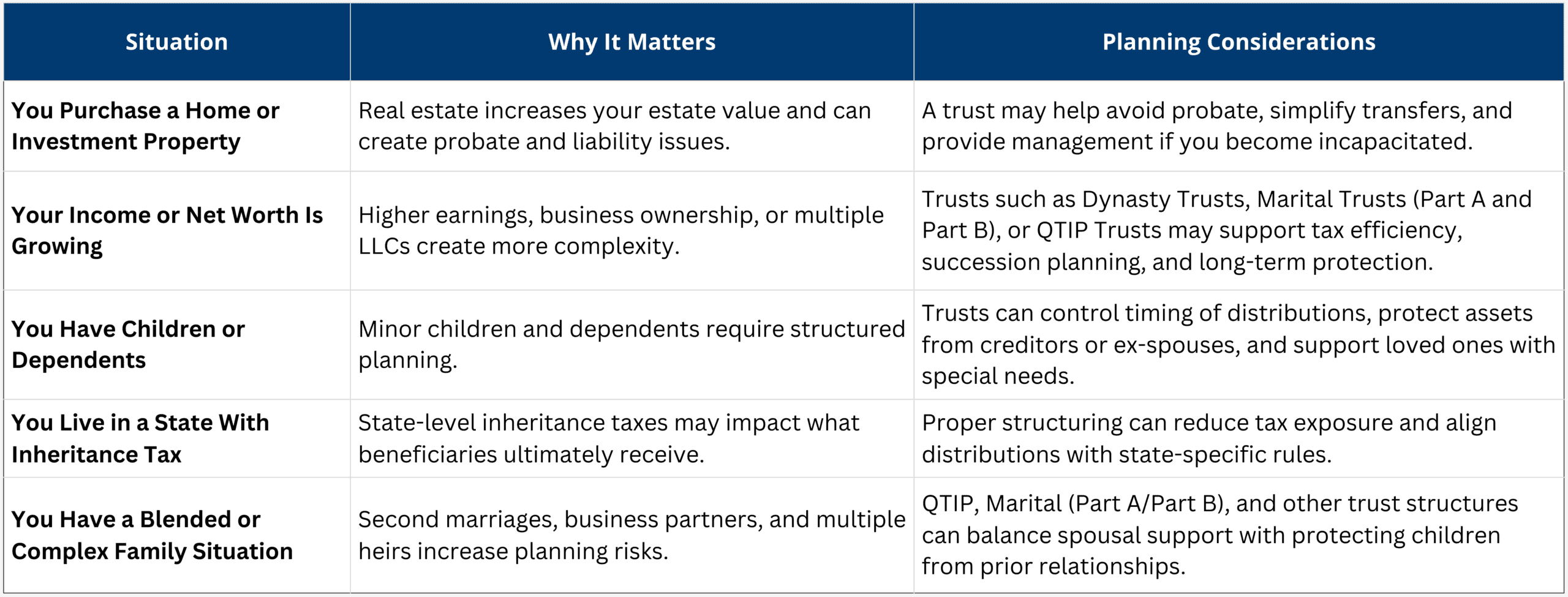

When should You Start the Conversation About a Trust?

Most people assume trusts are something to think about later in life. Later, when their net worth is higher. Later, when something major happens.

In reality, the right time to start the conversation is usually earlier than people think.

You do not need a dramatic life event or a seven-figure estate to begin planning. What you need is awareness that your financial life is becoming more complex.

As your financial life becomes more complex, certain milestones may signal it’s time to revisit your estate plan. You may not feel “wealthy,” but added responsibility often calls for added structure.

The following situations are common indicators that a trust conversation could be beneficial, even if you are simply exploring your options.

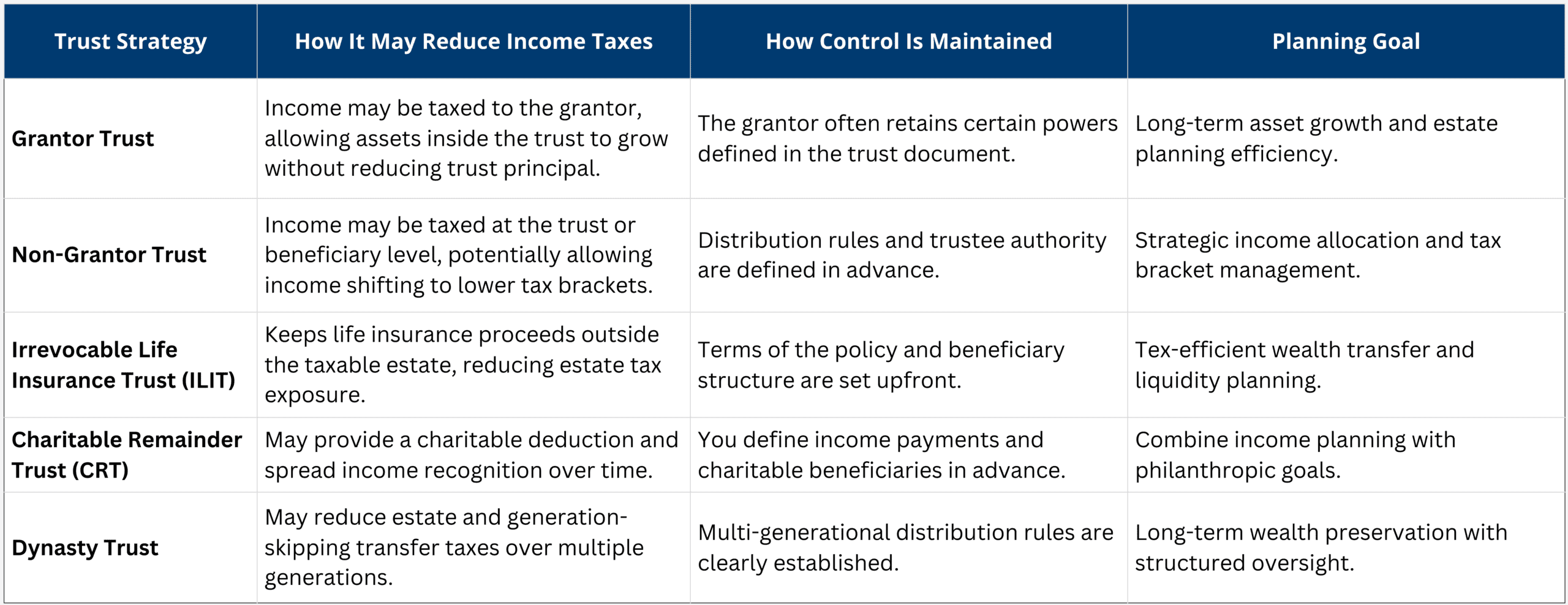

How can Trusts Reduce Income Taxes While Maintaining Control?

One of the biggest misconceptions about trusts is that you must give up control to gain tax benefits. However, many trust structures are designed to balance tax efficiency with clear decision-making authority.

Depending on how a trust is structured, income can be shifted, deferred, or managed to reduce overall tax exposure. In some cases, income is taxed at the beneficiary’s rate instead of the grantor’s. In others, distributions can be timed strategically to help manage tax brackets from year to year.

Below is a simplified overview of how different trust strategies can support tax planning while preserving structure and oversight.

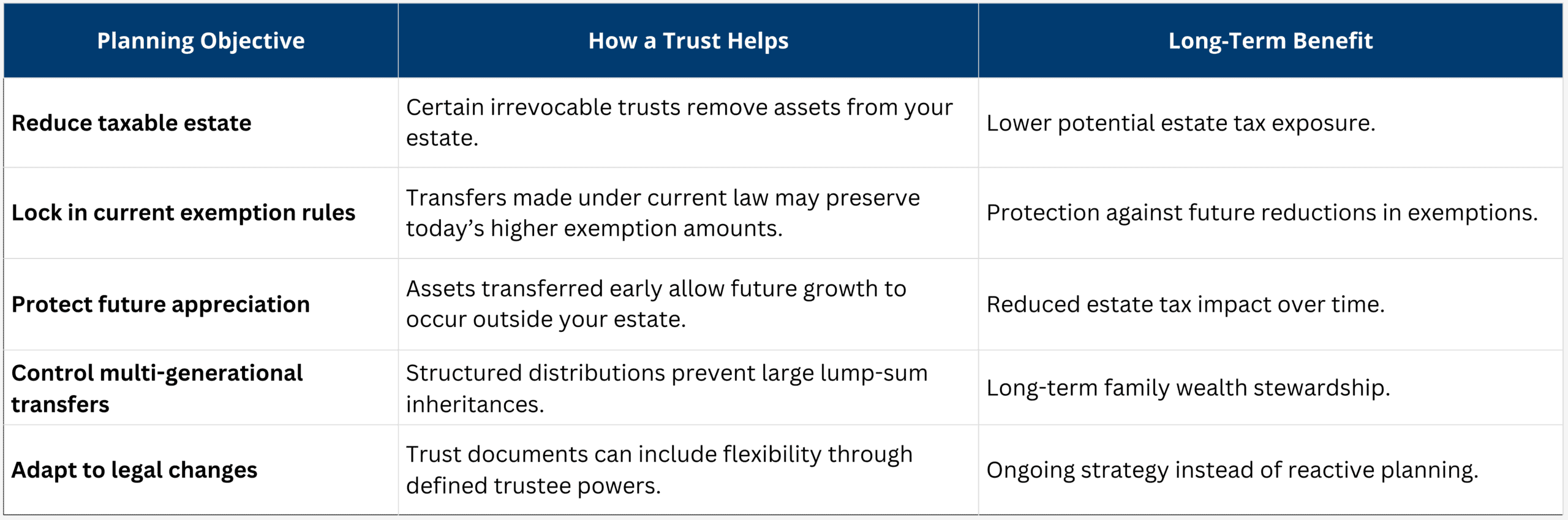

What Role Do Trusts Play in Estate and Gift Tax Planning as Rules Change?

Tax laws change. Exemption amounts rise and fall. State rules shift. That uncertainty can create hesitation for families who want to plan but are unsure what the future holds.

Trusts provide stability in a shifting environment.

They allow families to implement strategies under current rules while maintaining flexibility to adapt later. In other words, trusts are not a one-time solution. They are part of an ongoing planning framework.

From an estate planning perspective, trusts can

-

- Remove assets from a taxable estate.

- Protect future asset appreciation from estate taxes.

- Transfer wealth gradually instead of in one lump sum.

- Create structure across multiple generations.

When laws change, families who have already planned often have more options than those starting from scratch.

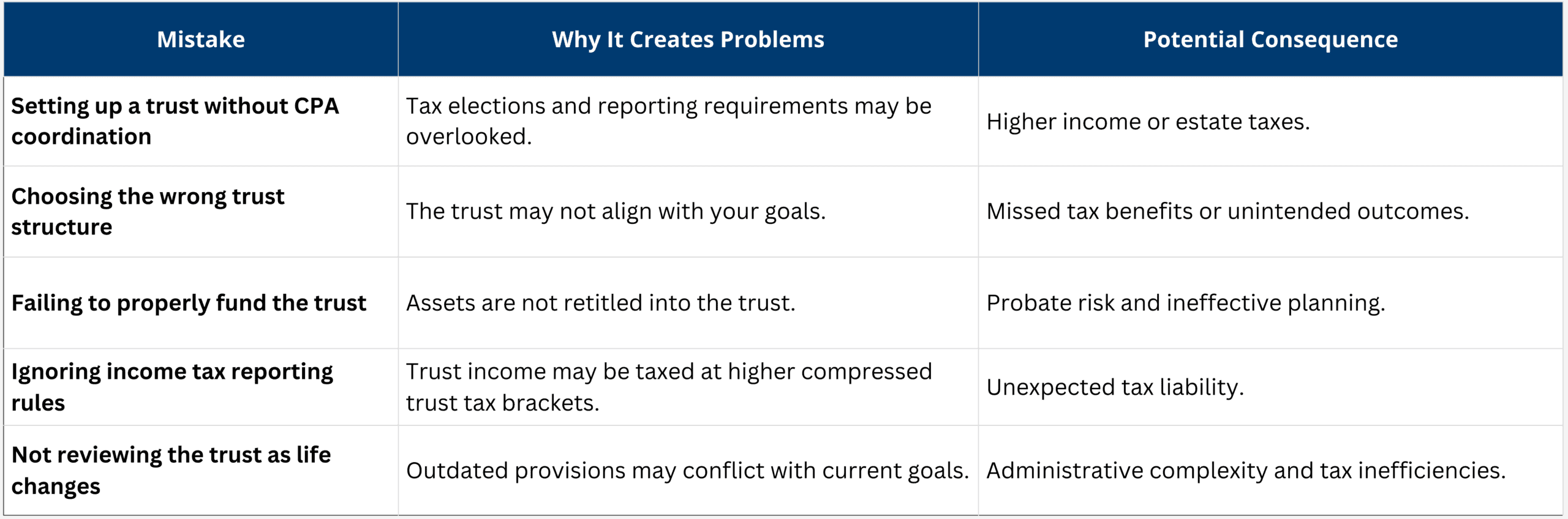

What Are the Most Common Tax Mistakes People Make with Trusts?

One of the most common mistakes is viewing a trust as simply a legal document rather than a tax-planning tool.

A trust affects income reporting, estate taxes, gift taxes, and sometimes state-level taxation. When established without coordination between legal and tax advisors, unintended consequences can arise.

Another frequent issue is selecting the wrong type of trust for the intended goal. Even a well-drafted trust can create problems if it is not properly funded or regularly reviewed.

The common theme is not that trusts create problems. Is it that poorly coordinated planning does.

When legal strategy and tax strategy work together, trusts can serve as powerful tools for income management, estate efficiency, and long-term family protection.

Here are common mistakes that often lead to unnecessary tax exposure.

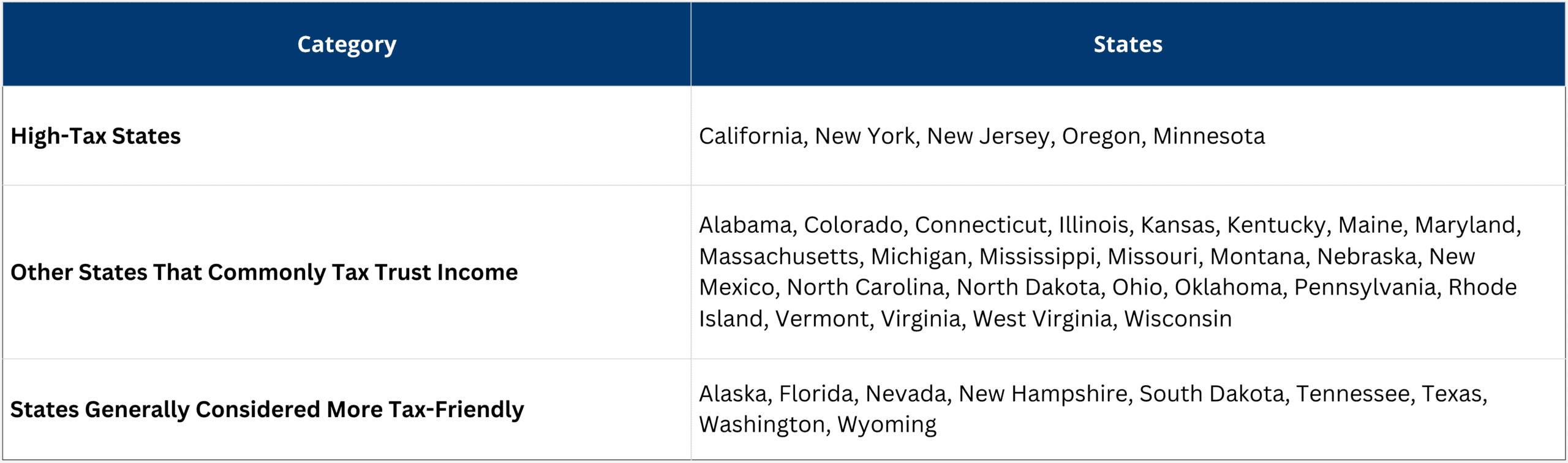

How Do States Tax Trust Income?

When families think about trust taxation, they often focus on federal rules. However, state income tax can have just as much impact, especially for non-grantor trusts.

Most U.S. states tax non-grantor trust income if the trust is considered a “resident” trust. Residency is not always straightforward. It can depend on where the trust is administered, where the grantor lived when the trust was created, or where the trustee or beneficiaries reside.

In high-tax states, this can significantly reduce after-tax income inside the trust. In contrast, certain states impose little or no income tax on trust income, making long-term planning more flexible.

For families with multistate connections, business interests, or trustees in different locations, state-level trust taxation can materially affect after-tax returns.

Thoughtful planning may involve reviewing:

-

- Where a trust is administered,

- Trustee selection,

- Distribution strategies, and

- Ongoing nexus considerations.

Because state trust tax laws are complex and often influenced by court rulings, planning should be carefully coordinated.

Disclaimer: State tax laws for trusts are highly complex and subject to change due to legislative updates and court decisions on nexus and residency. Regular review with qualified legal and tax advisors is essential.

Below is a simplified overview.

The Bigger Perspective

Trusts are not just for the ultra-wealthy. They are practical tools that can help manage taxes, protect beneficiaries, and bring clarity to long-term financial planning.

The key is coordination. A trust should align with your income strategy, estate plan, and evolving family circumstances.

If your assets are growing or your financial life is becoming more complex, this is a good time to start the conversation.

Let’s talk.

A thoughtful conversation can help determine whether a trust aligns with your goals and what type makes the most sense for your situation. Contact LGA to schedule a planning discussion and determine whether a trust strategy fits your goals.